/saur-energy/media/member_avatars/2025/09/24/2025-09-24t074149214z-whatsapp-image-2025-09-24-at-131104-2025-09-24-13-11-49.jpeg )

Follow Us

Follow Us

/saur-energy/media/media_files/2025/07/22/not-just-a-slowdown-5-things-europes-energy-deal-market-revealed-in-h1-2025-2025-07-22-16-14-04.png)

The first half of 2025 saw the Power Purchase Agreement (PPA) market face a noticeable downturn in Europe. But the headlines don’t tell the whole story. Amid an overall dip in PPA volumes, certain technologies and regions bucked the trend, and Battery Energy Storage Systems (BESS) emerged as a game-changer.

Here are five key trends drawn from Pexapark PPA Times – July 2025 Edition, that paint a full picture of the PPA and BESS landscape in Europe in early 2025.

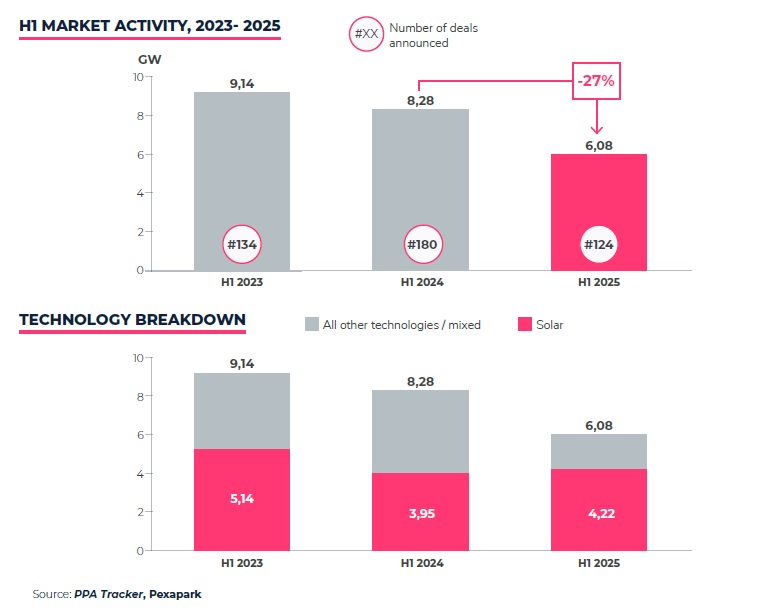

#1 PPA Volumes Decline Over 25% – But Not Everywhere, Not Solar

Global PPA activity cooled compared to the frenzy of 2024. Across 124 deals, just over 6 GW of renewable capacity was contracted under PPAs in H1 2025, a 26 percent drop in volume and 31 percent fewer deals than the same period in 2024. The chart shows H1 total PPA volumes for 2023, 2024, and 2025, with solar vs other technologies.

Interestingly, the average deal size actually increased to about 48.2 MW, a 5 percent increase compared to a year earlier, hinting at a shift toward larger projects even amid the slowdown.

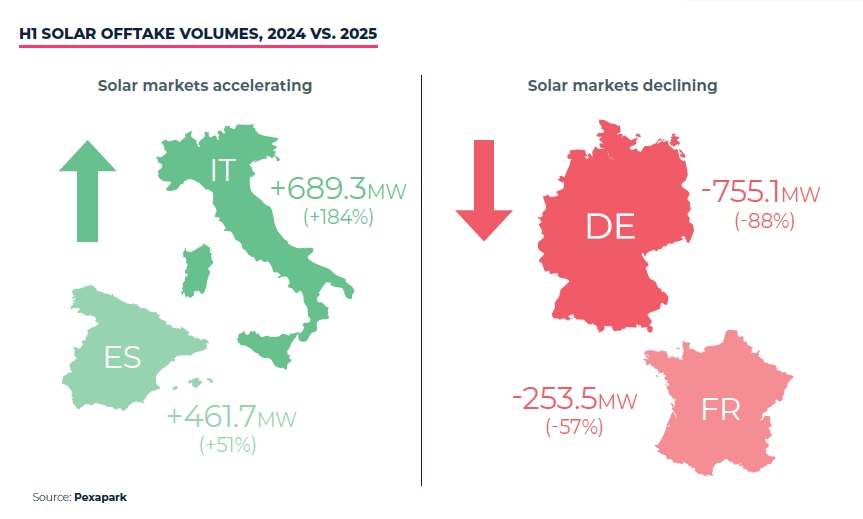

The decline wasn’t universal across markets or technologies. In fact, solar PPA volumes slightly increased year-on-year - 4.2 GW in H1 2025 vs 3.9 GW in H1 2024. The pullback came mainly from other segments like offshore wind, which plunged to just 0.13 GW from 0.54 GW in H1 2024.

On the contrary, some markets, especially Germany and France, also hit pause on new solar deals. Germany saw the largest decline in volumes with solar PPA volume falling a dramatic 84 percent YoY amid cannibalization concerns. But Southern European countries, like Italy, picked up the slack as solar PPAs surged by 184 percent, adding about 700 MW more than last year.

In short, overall PPA investment is down, yet mature markets and solar-heavy regions are proving resilient, suggesting the dip is more of a recalibration than a freefall.

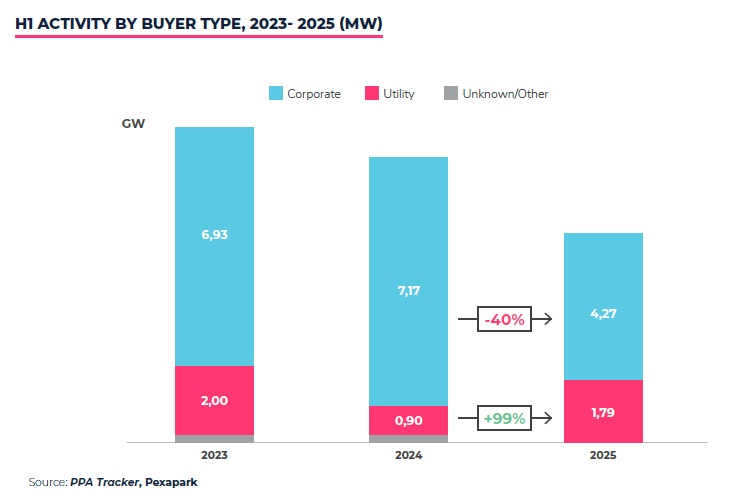

#2 Corporate Buyers Pull Back, While Utilities & Traders Step Up

Corporate PPA procurement hit the brakes in early 2025, while utilities and energy traders showed positive uptick at the opportunity.

Corporations contracted roughly 4.3 GW via PPAs in H1 - with 94 deals - over 40 percent less volume than H1 2024’s ~7.2 GW. Their hesitation stems from new market risks, that is the rise of negative power prices, uncertainty in pricing future solar “cannibalization” effects, and a mismatch between solar production peaks and companies’ consumption patterns.

By contrast, utilities doubled their PPA take - about 1.8 GW across 28 deals, versus 0.9 GW a year earlier. Being in the business of managing risk, traders and utility companies are more comfortable taking on these challenges and even see opportunity in them.

Notably, battery storage is aiding this shift, with BESS providing a natural hedge against solar output volatility, utilities are eagerly integrating storage and snapping up solar PPA volumes that corporates shy away from.

The silver lining is that PPA pricing has become a bit more realistic, narrowing the gap between what cautious buyers will pay and what sellers ask.

Notably, new entrants haven’t disappeared as 53 first-time corporate off-takers and 11 first-time utilities signed deals in H1 2025, proving there’s still a steady stream of fresh demand for clean energy PPAs.

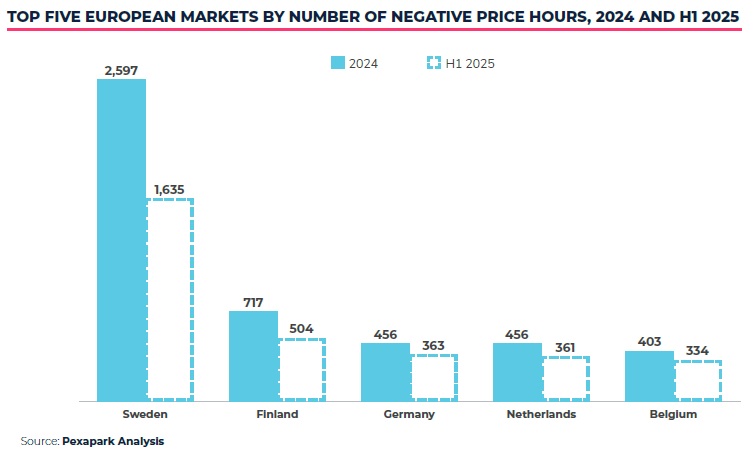

#3 Negative Power Prices Surge, Clouding PPA Economics

Episodes of negative electricity prices are multiplying alarmingly, and 2025 is on track to smash records. In markets with high renewable penetration, power prices fell below zero so frequently that by mid-year many countries had reached ~67 percent of their total 2024 negative-price hours.

For instance, Norway has already hit 90 percent of last year’s count, Denmark 87 percent, and Spain 86 percent. Sweden still tops the leaderboard for the most negative-price hours, with Finland, Germany, the Netherlands, and Belgium not far behind. This trend is directly impacting PPA valuations.

More hours of zero or negative prices mean lower capture rates for renewable projects, especially solar, and greater uncertainty in long-term PPA price setting. Deals now hinge on how this risk is shared. Contracts are seeing wide price differences depending on whether the buyer or seller bears the brunt of these negative-price periods. The industry is only beginning to move toward a consensus on how to price this new risk.

So far, one clear pattern is emerging - solar PPAs are being discounted more steeply than wind, reflecting investors’ wariness of midday price cannibalization. As negative-price events mount in 2025, figuring out how to manage this volatility is becoming a critical piece of PPA negotiations.

#4 Price vs Value: PPA Green Premiums Start to Fade

Many recent PPA deals priced well above ‘fair value’ are now facing a reality check. The Pexapark illustration based on German solar PPA data suggests that the gap between transactable PPA prices and the risk-adjusted fair value is closing as buyer bids and seller offers converge.

For the past few years, some buyers were willing to pay top-dollar premiums for green energy PPAs. In the PPA arena, that gap between price and value had widened, with corporates paying an extra ‘green premium’ to claim new-build renewable projects and additionality. H1 2025 marked a turning point.

In markets like France, transactable PPA rates were reported up to €15/MWh above what Pexapark considered a fair risk-adjusted price for a 15-year solar PPA, starting in 2027. Such cases have become harder to close as utilities often get priced out by those lofty offers.

Now two trends are underway. First, PPA price ranges are narrowing, indicating buyers and sellers are less far apart, but also less certain, as everyone cautiously tests the waters. When the gap was wide, at least one side was happy. Now, with ranges tighter, reaching agreement is trickier.

Second, ‘Transactable’ prices are drifting down toward fair value. Many corporate buyers have scaled back their budgets. They are no longer willing to pay just any price for green credentials. The result is a more disciplined PPA market heading into late 2025, one where pricing better reflects the actual risks and rewards of projects, rather than exuberant demand. In sum, the era of “green at any price” appears to be over, as of now, the economic reality sets in.

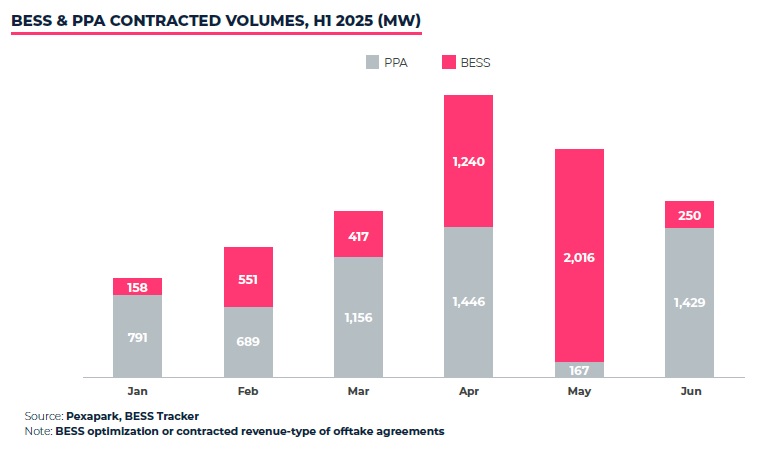

#5 Battery Storage Deals Skyrocket

If one segment utterly defied the PPA slowdown, it’s battery storage.

The BESS market has shown an impressive growth in early 2025, reaching levels that surpass the entirety of 2024’s activity. In the first half of 2025 alone, 4.6 GW / 9.2 GWh of battery storage capacity was signed under revenue contracts across 36 deals. That’s more than triple the volume of storage deals seen in all of 2024, which had about 1.6 GW / 3 GWh.

In just six months, BESS deal count also beat the full-year 2024 count by 44 percent, indicating that a new market is coming into its own.

The growth was powered by a wave of agreements in the two leading storage markets, Great Britain and Germany, and notably first-ever storage deals in countries like Belgium, Poland, Greece, and Bulgaria.

Early projects mostly feature two-hour batteries, with some moving to 3-4h durations. Bigger projects are embracing ‘bankable’ contract structures. For example, H1 saw four major tolling agreements over 200 MW each, and two floor-price deals covering 1 GW of capacity.

At the same time, storage developers are also comfortable going fully merchant with specialized algorithmic trading. Merchant storage deals made up about 2.5 GW of capacity in H1 2025, up from just 0.41 GW in 2024.

There’s also a trend toward portfolio-level deals, reaching up to 3 GW in H1, bundling multiple battery sites to diversify risk for financiers.

All these signals point to an increasingly mature storage sector now complementing the PPA space. In fact, the integration of BESS with renewables is blurring the line between generation and flexibility, this theme is going to persist. While the first half of 2025 may have been challenging for traditional PPAs, it belongs to battery storage, which is rapidly expanding the clean energy toolkit.